The era of easy Arab money and of oil that has only just started getting cheaper is ending, and the Persian Gulf already knows it and is switching to an entirely new game. In Poland this is discussed far too rarely, even though it will decide our energy sector and our place in the world for years to come. Meanwhile we are still asleep, and Africa – I am saying this on our channel for the third time now – will not wait for us.

Oil dear today, cheap tomorrow.

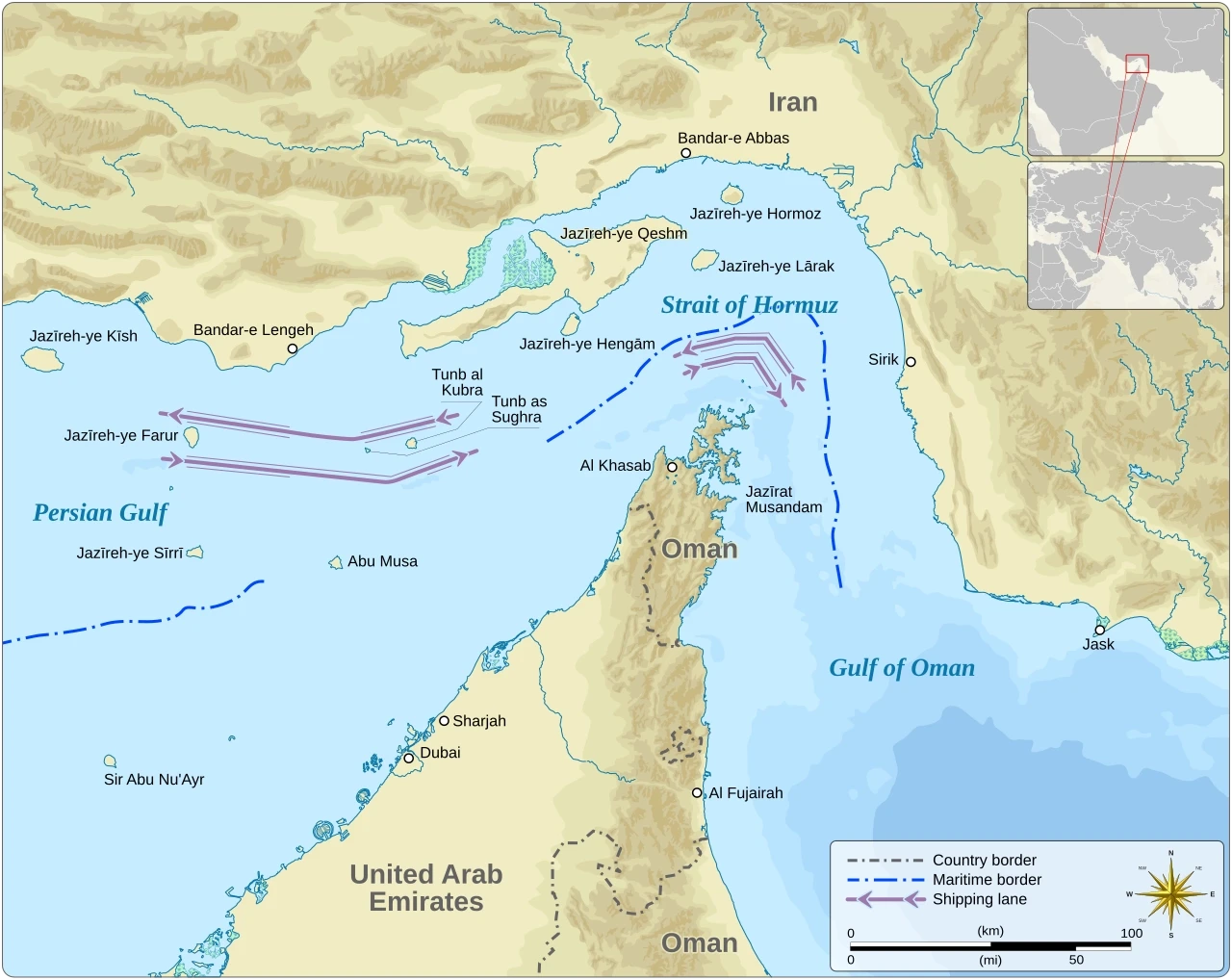

Let's start with the price, because it misleads. Today a barrel of Brent crude costs around $96, but that price is artificially inflated, because since the end of February Iran has in practice blockaded the Strait of Hormuz, through which something like a fifth of the world's oil flows. That is a fear premium, not a fundamentals premium. And the fundamentals say exactly the opposite. The American agency EIA forecasts that as early as next year the average price will fall to around $80 and will keep sliding towards $70 as the market calms down. Because demand for oil is slowing — the International Energy Agency expects it to plateau around 2030, and electric cars alone will push more than 5 million barrels a day off the market. To put it plainly — today's high price is the market's last twitches, not a lasting trend.

The Emirates leave OPEC, or the cartel cracks.

And here we come to something many in Poland missed. At the start of May this year the United Arab Emirates formally left OPEC. This is no trifle, this is a crack in the very heart of the oil cartel. The reason is purely arithmetical. The Emirates have built production capacity on the order of almost 5 million barrels a day, while the cartel quota held them at three and a half million — meaning close to a third of their potential stood idle. On top of that, the break-even thresholds for Gulf budgets are now radically different. Saudi Arabia, to balance its budget, needs oil well above $90, whereas the Emirates or Qatar close theirs already at fifty or sixty. And it is precisely this gulf that is the motive for the split — Riyadh defended the cuts and a high price, while Abu Dhabi simply wants to pump as much as possible. A country that plays for a fall and walks out of the cartel in order to extract without limit is, for oil prices, an unambiguous signal.

The end of easy Arab money.

The Arabs are not naive and are the first to see where this is heading. That is why the whole philosophy of their largest funds is changing. Adding up the wealth of the Gulf's sovereign funds, we are talking about a sum on the order of $5.5 trillion — that is about forty percent of all the world's wealth funds. Saudi Arabia's PIF, Abu Dhabi's ADIA, Kuwait's KIA, Qatar's QIA — each of them runs into the hundreds of billions, and the first two have already passed a trillion dollars. It used to be easy Arab money — all you had to do was show a bauble and say it was worth millions, and the sheikh would buy. Those days are ending. Today the Arab funds look at the rate of return and demand a local share, so-called local content — production, technology and jobs at home, not passive stakes in other people's trophies. Saudi Arabia's PIF already places four-fifths of its wealth domestically and requires partners to move production to the Kingdom. This is money that has become demanding.

The technology that eats oil.

The third force is technology, and here, as it happens, the most is going on. Oil is being replaced ever more boldly in new applications, especially in the energy sector. We are talking about hydrogen — the low-emission kind, today still most often "blue", but increasingly "green" — and about ammonia made from that hydrogen, which has turned out to be a convenient way of transporting it by ship. Japan already co-fires ammonia in its coal-fired power plants and is aiming for three million tonnes a year by 2030. And from that same gas, instead of burning it or refining it into fuel, one can extract ethylene and propylene, the building blocks of all plastics. In other words — the world is learning to do everything with hydrocarbons except burn them in a tank, and every such technology takes another slice of the market away from oil.

Africa will not wait.

And I come to a matter I keep stubbornly repeating. Africa will not wait for the moment when Poland or Europe finally wake up. The best example is Mozambique. Sitting on the gas deposits there are the world's biggest players — France's TotalEnergies, America's ExxonMobil and Italy's Eni. Last November TotalEnergies lifted force majeure on its huge project in Cabo Delgado province and in January resumed construction, with the first gas due to flow around 2029. Once all the projects are added up, Mozambique stands a chance of becoming one of the world's significant exporters of liquefied gas, and the largest in Africa, as early as the start of the next decade. On top of this there is the African race for green hydrogen — from Egypt, through Morocco and Mauritania, to Namibia and South Africa. Not everything there works out, some projects stumble over a lack of buyers, but the direction is a single one. Africa is arming itself with the energy of the future, while we are still debating whether it is even worth it.

Catching the train

This whole puzzle assembles into a single picture. The cheap oil now approaching is not a gift — it is a warning that the age of easy fuel and easy fuel money is drawing to a close. The smartest players, those of the Gulf, have already switched — from trophies to return on capital, from quotas to maximum production, from oil itself to hydrogen, gas and technology. The question is not whether the world will change, because it is changing before our eyes. The question is whether we will make it onto that train, or whether we will watch it pull away with Arab capital and African gas on board. Because I will say it once more, as calmly as I can — Africa will not wait.

In this piece I draw on the oil price forecasts of the American agency EIA and on the demand analyses of the International Energy Agency, on the circumstances of the United Arab Emirates' exit from OPEC in May this year and on data about the break-even thresholds of Persian Gulf states' budgets, on the estimates of the value of the Gulf's sovereign wealth funds published by Global SWF, on the strategy of the Saudi PIF fund, on Japanese ammonia co-firing programmes, and on the status of the gas projects in Mozambique run by TotalEnergies, ExxonMobil and Eni.